+91 7014607737

+91 7014607737

info@technoloader.com

info@technoloader.com

Table of Contents

Key Takeaways:

- Blockchain is simply a decentralized and immutable digital ledger that records transactions safely over multiple nodes, which removes the need for intermediaries.

- The technology has transformed over 30+ years, from early cryptographic concepts to becoming a main digital infrastructure in 2026.

- Blockchain operates through a step-by-step process that includes transaction initiation, network verification, block creation, consensus mechanisms, and permanent recording on the chain.

- Key components such as nodes, the distributed ledger, transactions, consensus algorithms, and cryptographic hashing bring security, transparency, and data integrity.

- There are four types of blockchain networks, which include public, private, consortium, and hybrid. Each blockchain network type is particularly designed for different levels of access, control, and use cases.

- Blockchain is transforming several industries, including finance, supply chain, healthcare, real estate, voting systems, education, and energy trading, by improving transparency and efficiency.

- The future of blockchain typically lies in integration with AI, CBDCs, and decentralized systems, which makes it a base layer for the next generation of digital infrastructure.

Introduction

Imagine there is a digital notebook that thousands of people over the world hold a copy of. Every time someone writes a new entry, everyone’s copy updates spontaneously. And, no one can secretly delete or edit, even with a single line of code. Not even the person who wrote it.

That’s blockchain technology! And it’s bigger than most people realize. The global blockchain market is projected to reach $47.96 billion in 2026 and is growing every year.

You’ve probably heard the word thrown around in conversations about Bitcoin, cryptocurrency, or digital payments. But in 2026, blockchain is no longer just the backbone of crypto. It is now reshaping how governments store land records, how hospitals protect patient data, and how global companies track products from factory to your doorstep.

Yet, for most people, it remains one of those “I’ve heard of it but don’t really get it” technologies.

Today, you’ll understand everything about it.

By the time you finish reading, you will clearly understand:

- What blockchain is

- How it works, step by step

- Why its regarded as one of the most important technologies of our time?

- And more.

Let’s start from the very beginning!

What Is Blockchain?

Blockchain is a revolutionary technology that basically functions as a shared and immutable digital ledger. Its name comes from the structure of data that is organized in blocks, with each new block connected to the prior one. This creates a chain.

Each block contains essential data, including a list of transactions, a timestamp, and a unique identifier known as a cryptographic hash. Well, this hash is generated from the contents of the block and the hash of the previous block. This ensures that each of the blocks is well connected to the one before it.

Blockchain is both distributed and decentralized, meaning that no single authority can gain control over it. Instead, multiple nodes within the network maintain their own copies of the blockchain, keeping the ledger synchronized. This guarantees that once data is recorded, it becomes permanent and cannot be changed or deleted.

A Brief History of Blockchain

Blockchain technology didn’t just appear overnight. It has been built for more than over three decades. Here’s how it all happened:

- 1991: Two research scientists named Stuart Haber and W. Scott Stornetta introduced the concept of blockchain. They wanted a solution for time-stamping digital documents so that they could not be tampered with or misdated. Using cryptography, they developed a system where time-stamped documents were stored in a chain of blocks. This was the very first blueprint of blockchain technology.

- 1992: Shortly after, Merkle Trees, which was a mathematical data structure, were incorporated into the system developed by Haber and Stornetta. This made the technology more efficient, as multiple document records could now be collected and stored in a single block using a secured chain.

- 2000: In 2000, cryptographer Stefan Konst published his theory of cryptographically secured chains, along with practical ideas for how such a system could actually be implemented in the real world.

- 2004: Cryptographic Hal Finney introduced Reusable Proof of Work (RPoW). His system solved the famous “Double Spending Problem,” which refers to the risk of a digital currency being spent more than once. He did this by keeping the ownership of tokens registered on a trusted server, which ensured each token could only be used once.

- 2008: After that in 2008, Satoshi Nakamoto published a whitepaper titled “Bitcoin: A Peer-to-Peer Electronic Cash System.” In it, he introduced the concept of a Distributed Blockchain, which was a modified version of Merkle Tree that was far more secure. His system used a peer-to-peer network for time-stamping transactions.

- 2009: In 2009, Nakamoto released the Bitcoin whitepaper to the public and mined the first block, known as the Genesis Block. Bitcoin began trading, and the blockchain era officially began. A British IT worker named James Howells even began mining Bitcoin. He spent almost $17,000 on it. Back in 2013, while he was cleaning his house, he accidentally discarded a hard drive that had his Bitcoin wallet on it. Now, those Bitcoins are worth $127 million, and they’re still unclaimed.

- 2014: This year marked a turning point. Blockchain technology was formally separated from cryptocurrency, which gave birth to what is known as Blockchain 2.0. Financial institutions and other industries began recognizing that the underlying technology had far greater potential than just digital currency.

- 2015: The Ethereum blockchain network was launched, which enabled developers to write smart contracts and decentralized applications (dApps) on a live network for the first time. In the same year, the Linux Foundation launched the Hyperledger project, which was an open-source initiative to advance blockchain technology for enterprise use.

- 2016: Up until this point, “block” and “chain” were used as two separate words. In 2016, the term “blockchain” was officially accepted as a single word. The same year, a bug in the Ethereum DAO smart contract code was exploited by a hacker, which resulted in a hard fork of the Ethereum network. Also, the Bitfinex Bitcoin exchange was hacked, which lead to the theft of 120,000 Bitcoins.

- 2017: Japan officially recognized Bitcoin as a legal currency, which gained global acceptance of blockchain-based assets. The same year, Block.one introduced the EOS blockchain operating system, designed specifically to support large-scale and commercial decentralized applications.

- 2020: Stablecoins gained popularity, as they offered the benefits of blockchain without the wild price swings of regular crypto. Ethereum also launched the Beacon Chain, the first major step toward Ethereum 2.0 and a more energy-efficient future.

- 2022: Ethereum completed one of the most significant technical upgrades in blockchain history, that is, The Merge. The original Ethereum mainnet merged with the Beacon Chain, which transitioned from Proof of Work (PoW) to Proof of Stake (PoS). And as a result, Ethereum’s energy consumption dropped by approximately 99.95% overnight.

- 2023: Generative AI made its mark on the blockchain industry. This opened up entirely new possibilities for how blockchain applications could be designed, automated, and scaled. Blockchain was also heavily used this year as the backbone of digital identity networks, with governments worldwide launching digital ID solutions. The EU passed its landmark MiCA regulation, which was the first legal framework for crypto assets in Europe.

- 2024: By 2024, the Bitcoin blockchain alone had grown beyond 600 GB, which shows how much activity had been recorded on the network. And, institutional adoption rose.

- 2025-2026: Blockchain has now crossed from emerging technology into foundational digital infrastructure. Over 130 countries are now exploring Central Bank Digital Currencies (CBDCs). AI and blockchain are increasingly being used together to power autonomous smart contracts and decentralized computing systems.

How Does Blockchain Work?

Understanding how blockchain works is quite simpler than it sounds. The below is an example:

Meet Jack and Danny. They are basically nodes on the Bitcoin network. Jack has to send 20 BTC to Danny. This is what happens when he initiates the transfer:

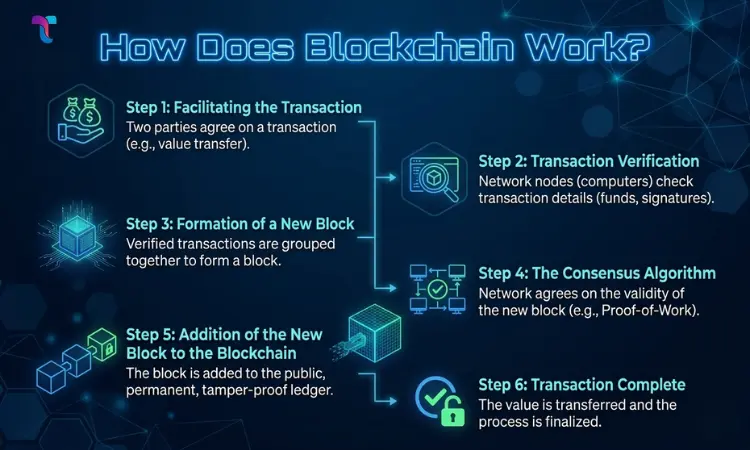

Step 1: Facilitating the Transaction

Jack opens his Bitcoin wallet and initiates to send 20 BTC to Danny. As soon as he does this, a transaction request is created and spread to the entire Bitcoin network. This request is transferred to every node in the network.

Step 2: Transaction Verification

When the transaction request reaches the network, every node begins the verification process. They verify:

- Does Jack have 20 BTC in his wallet to fulfill this transaction?

- Is Jack registered as a node on the network?

- Is Danny a registered node on the network?

The network only gives the transaction a green signal when all these parameters are validated.

Step 3: Formation of a New Block

A verified transaction is not added to the blockchain spontaneously. Instead, it remains in a holding area, called the mempool, where it sits alongside hundreds of other verified transactions. When there are enough transactions, they are combined and saved in one unit called a block. The transactions of both Jack and Danny are now part of this block.

Step 4: The Consensus Algorithm

Since we are talking about Bitcoin, the network uses the Proof-of-Work (PoW) consensis mechanism to verify this new block before it can be added to the chain.

In PoW, the system assigns a target hash value to the network. Miners compete against each other to calculate a hash value for the new block. It is a race to solve a complex mathematical puzzle. The first miner who solves it can add the block to the blockchain and is rewarded with Bitcoin. The rest are called stale blocks.

Step 5: Addition of the New Block to the Blockchain

When the block has been checked through PoW and assigned its hash value, the new block is connected to the open end of the existing chain, which links itself to the prior block through its hash. Every node on the network updates its copy of the blockchain. The transaction of Jack and Danny is now an unalterable part of the Bitcoin blockchain.

Step 6: Transaction Complete

As soon as the block is added, the transaction is complete. 20 BTC transfers from Jack’s to Danny’s wallet. The details of this transaction, such as who sent it, who received it, how much, and when, are now permanently secured on the blockchain for anyone to see and check.

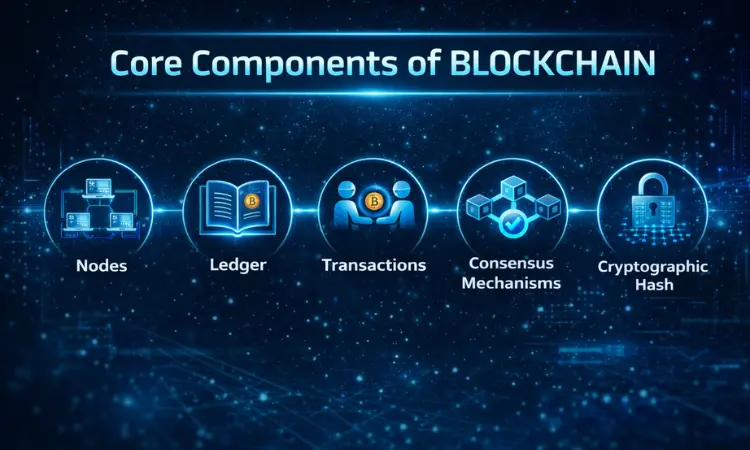

Core Components of Blockchain

The main elements of blockchain are important for their operation and functionality. The below mentioned are explanations of each:

Nodes

Nodes are basically individual computers that participate in the blockchain. Each node keeps a copy of the entire blockchain or a part of it.

Ledger

The blockchain itself serves as a distributed ledger that records all transactions in a safe and immutable manner. It is composed of blocks, each of them contains a set of transactions, a timestamp, and a hash to the prior blockchain. This forms a chronological chain.

Transactions

Transactions are the basic units of data in a blockchain, which represent the transfer of value or information. A transaction is created, verified by nodes, and then securely recorded on the blockchain. And, it even includes the sender’s or receiver’s addresses, the amount, and a digital signature.

Consensus Mechanisms

Consensus mechanisms are simply algorithms that help the network to agree on the validity of transactions and keep a consistent state of ledger. Some consensus mechanisms include PoW, PoS, and DPoS.

Cryptographic Hash

Cryptographic hash is the core element within the blockchain industry. It serves as a crucial tool to ensure the integrity and security of data. Hash takes input data of any size and produces a fixed-size string of characters.

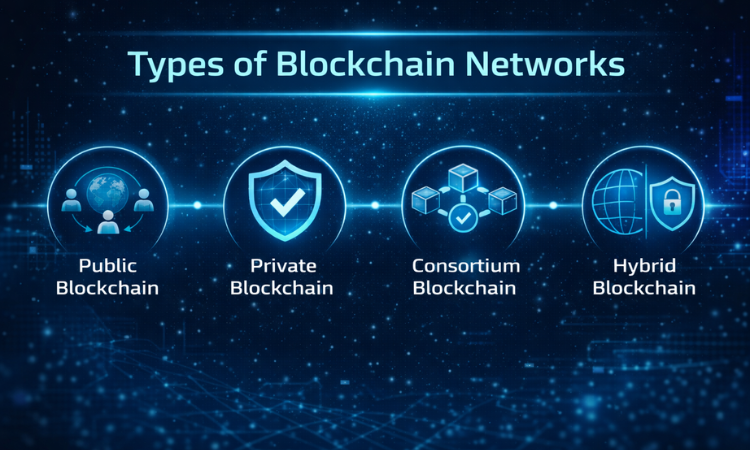

Types of Blockchain Networks

Not all blockchains are built the same way. They differ in access, control, and purpose. The following are the four main types!

Public Blockchain

A public blockchain is open to everyone. Anyone with an internet connection can join the network, view the transaction history, participate in the validation process, and carry out transactions. There is no permission or identity verification needed.

Bitcoin and Ethereum are well-known examples of public blockchains. They are decentralized, secure, and transparent. Public blockchains might be slower and consume more energy because multiple nodes must verify each transaction.

Private Blockchain

A private blockchain typically functions within a closed environment. Access is limited and regulated only by a single organization. Only authorized participants can join the network, view data, or conduct transactions.

It offers advantages over traditional databases, including immutability, an auditable transaction history, and enhanced internal security. Hyperledger Fabric, built under the Linux Foundation, is one of the well-known private blockchain frameworks.

Consortium Blockchain

A consortium blockchain is a type of blockchain that falls between public and private blockchains. Rather than being managed by just one organization, it’s overseen collectively by a group of organizations that have come together to collaborate on a shared network.

For example, a group of banks could form a consortium blockchain to process interbank transactions faster and safely. R3 and Quorum are examples of consortium blockchains that are used in the banking and finance sector.

Hybrid Blockchain

A hybrid blockchain mixes the elements of both public and private blockchains. Businesses using a hybrid blockchain can even choose which type of data to make publicly visible and which data to keep restricted. This also gives them the flexibility to enjoy the transparency of a public blockchain while maintaining control over sensitive information.

Dragonchain, originally developed by Disney, is one of the earliest examples of a hybrid blockchain. Today, hybrid blockchains are gaining popularity in government applications and healthcare, where certain records must be publicly verifiable while others must remain confidential.

Real-World Applications of Blockchain

For a long time, blockchain was associated with Bitcoin and cryptocurrency. That perception has changed dramatically. Today, blockchain is quietly working behind the scenes across industries — solving real problems that traditional systems have struggled with for decades.

Here are the most significant real-world applications of blockchain technology in 2026.

Finance & Banking

Finance was the first industry blockchain disrupted, and it remains the largest adopter to this day. Financial services accounted for 46% of global blockchain market revenue in 2025 and that share continues to grow.

Traditional cross-border payments are slow, expensive, and dependent on multiple intermediaries. A simple international wire transfer can take 3 to 5 business days and lose a portion of the amount to fees. Blockchain in banking helps eliminate the middlemen entirely. Transactions that once took days now settle in minutes, at a fraction of the cost.

Supply Chain Management

Supply chains are among the most complex systems in the world, which involve manufacturers, shippers, customs authorities, warehouses, and retailers. The lack of transparency in this system has led to fraud, counterfeiting, and massive inefficiencies.

Blockchain in supply chain helps solve this by creating a tamper-proof record of every step a product takes. IBM’s Food Trust platform connects retailers like Walmart to growers, which reduces food recall times from weeks to seconds. What previously required weeks of manual investigation to trace a contaminated food product now takes mere moments on blockchain.

Healthcare

Healthcare generates some of the most sensitive data in existence like patient records, prescription histories, diagnostic results, and clinical trial data. Managing this data securely, while making it accessible to the right people at the right time, has been a challenge for the industry.

Blockchain addresses this directly. Platforms like Medicalchain use blockchain to store patient health records securely, which allows patients to control access and share their medical data with healthcare providers. Beyond records, the use of blockchain in healthcare helps verify the authenticity of medicines and track pharmaceutical supply chains, which addresses the global problem of counterfeit drugs.

Voting & Governance

Democratic elections depend on trust. Citizens must trust that their vote was counted, that no votes were added or removed, and that the result reflects the actual will of the people. Traditional voting systems have struggled to provide this guarantee.

Blockchain-based voting systems offer a solution. Every vote is recorded as a transaction on the blockchain, which is immutable, timestamped, and publicly verifiable. Governments are already using blockchain for digital identity verification, land registry management, and secure voting systems.

Real Estate

Buying or selling property is one of the most paperwork-heavy, time-consuming, and fraud-prone transactions a person can make. Title fraud alone costs property owners billions of dollars every year worldwide.

Use of blockchain in real estate simplifies this. Property records stored on a blockchain cannot be altered or forged. Smart contracts can automatically transfer ownership the moment payment is confirmed, which eliminates the need for lawyers, notaries, and weeks of administrative delays. Property transactions recorded on a blockchain eliminate the need for paper-based records and reduce the risk of fraud.

NFTs & Digital Ownership

For most of the internet’s history, digital content could be infinitely copied. A photograph, a piece of music, or a digital artwork could be duplicated millions of times with no way to establish who the original creator was or who legally owned it.

Non-Fungible Tokens (or, NFTs) changed this. An NFT helps verify ownership and the original creation of a digital asset. This allows creators to sell their original digital artworks directly to buyers, while enabling buyers to verify originality and ownership history without relying on a third party.

Energy Trading

One of the lesser-known but rapidly growing applications of blockchain is in the energy sector. Blockchain enables individuals and businesses to trade renewable energy directly with each other, without going through a utility company.

In January 2025 alone, PowerLedger’s TraceX system facilitated over 1.2 million Renewable Energy Certificate trades on-chain, while integrating the immutability of blockchain with traditional energy registry systems. This peer-to-peer energy trading model has implications for how clean energy is distributed and monetized globally.

Education & Credential Verification

Fake degrees and forged certificates are a serious problem in hiring processes worldwide. Blockchain offers a permanent and secure solution. Academic institutions can issue certificates directly onto the blockchain, and employers can check them quickly, without needing to contact the institution or wait for a response.

The global blockchain in education market is estimated to reach somewhere around $13.52 billion by 2035, which is growing at a CAGR of 43.94%. This percentage is driven by institutions worldwide modernizing how credentials are issued, stored, and verified.

Conclusion

That brings us to the end of this blog!

Blockchain technology began as a way to fix a problem, that is, how to create trust between strangers without relying on a central authority. What started as the backbone of Bitcoin in 2008 has since grown into one of the technological shifts of the 21st century.

Over this blog, we have seen what blockchain is, how it works, its main components, its different types, and the industries it is transforming.

Understanding blockchain is just the beginning. The second step is getting to learn how to create with it.

If you are a business willing to use blockchain technology in your operations, be it developing smart contracts, launching a cryptocurrency, building a dApp, or creating a custom blockchain solution, having the right partner can really make a big difference.

Technoloader is a leading blockchain development company with more than 8+ years of experience in offering robust, scalable, and future-ready blockchain solutions. We can be your partner that can help you turn blockchain potential into real-world results.

Get in touch with us today!

Frequently Asked Questions

What is blockchain technology in simple terms?

Blockchain is a digital way to keep records. Data is kept in blocks that are linked together and stored on many computers around the world. Once information is recorded, no one has the right to change or delete it.

Is blockchain the same as Bitcoin?

No, Bitcoin is a cryptocurrency, which is a form of digital money. Whereas, blockchain is the technology that powers Bitcoin.

Is blockchain completely hack-proof?

Blockchain is one of the most secure technologies ever developed, but no technology is entirely hack-proof. What makes blockchain difficult to attack is its structure, and altering a single record would require simultaneously changing every copy of the blockchain across thousands of nodes worldwide.

What is the difference between blockchain and a regular database?

A traditional database is controlled by a single entity, such as a company, a bank, or a government, that has the authority to add, edit, or delete records. On the other hand, a blockchain is decentralized and immutable. No single entity controls it, and once data is recorded, it cannot be changed or deleted. This makes blockchain way more transparent and tamper-resistant than traditional systems.

Is it possible to delete blockchain data?

No. This is one of blockchain’s defining features, that is, immutability. When something is added to a blockchain, whether it’s a transaction or data, it stays there forever. Nobody can ever delete or change it. This is what makes blockchain so reliable for applications like financial records, legal documents, and identity verification.

What is the difference between blockchain and cryptocurrency?

Cryptocurrency is basically a digital currency that uses blockchain as its underlying technology to record and verify transactions. However, blockchain is a much broader technology with applications far beyond currency, including supply chain management, healthcare, voting systems, and more. Every cryptocurrency runs on a blockchain, but not every blockchain is used for cryptocurrency.

Deepa Manwani

Deepa Manwani is a Technical Content Writer at Technoloader with over 7 years of experience creating high-quality content across Blockchain, Web3, AI, and fintech. She specializes in translating complex technical concepts into clear, engaging, and informative content that helps businesses, developers, and users better understand emerging technologies. Her expertise includes writing technical blogs, technical documentation, whitepapers, platform guides, and in-depth content for crypto exchanges, DeFi platforms, trading systems, and enterprise software solutions. At Technoloader, she contributes to developing strategic content that supports product growth, strengthens brand credibility, and educates users about next-generation technologies shaping the future.

Published in Blockchain Development